Gross profit and contribution margin are two integral numbers for any manufacturing, wholesale or construction business. But what do they mean and why are they crucial? In this post we explore these two elements and how to bring them to life in your business.

In this article:

→ What is contribution margin?

→ What makes up contribution margin?

→ Variable COGS for a housing or construction business

→ Variable COGS for a manufacturing business

→ Formula to calculate contribution margin (in $ and %)

→ Contribution margin and economies of scale

→ How does gross profit fit in?

A Simple Guide to Contribution Margin & Gross Profit

“Contribution margin and gross profit: they’re two terms you may or may not have heard of. You’ve most likely heard of gross profit, but you may not have heard of contribution margin. They’re two really important numbers to understand if you’re running a construction, wholesale or manufacturing business.

What is contribution margin?

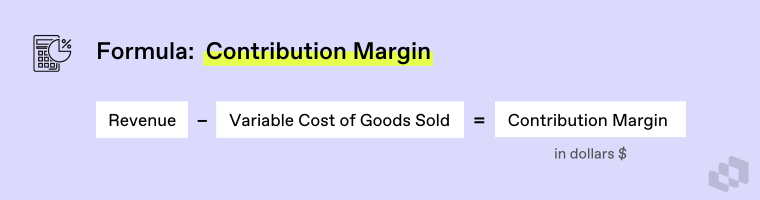

Contribution margin is looking at your revenue minus your variable cost of goods sold (COGS). It’s an accounting calculation that tells you how much a certain product contributes to your business's overall profit.

Now let’s look at the definitions of each of those components to understand what makes up contribution margin as a whole.

- ‘Revenue’ – This is the money from what you sell, from doing what you do.

- ‘Variable’ means that they should move (that is, being variable: up and down) as you sell more or less of a product.

- ‘Cost of goods sold’ means it’s directly tied to what you’re doing.

→ Related: A Simple Guide to Contribution Margin

Let’s look at a couple of examples.

Variable COGS for a housing or construction business

A variable cost of goods sold for housing or a construction business would be things like steel beams, bricks, the concrete, which goes into manufacturing a house. They will, all the more you sell, increase or the less you sell decrease. If you’re looking at a wholesale business, if I’m in a wholesale business selling laptop computers, my variable cost of goods sold will be the laptops themselves, and also the freight to get them into our possession and into our stores or to our client.

Variable COGS for a manufacturing business

If you’re a manufacturing business, let’s say you manufacture wooden furniture. It would be the cushions, it would be the wood that goes into the furniture; they’re your variable costs of goods sold, as very simple examples.

How to calculate contribution margin

To work out the contribution margin (in dollars), simply subtract your variable costs of goods sold from your revenue.

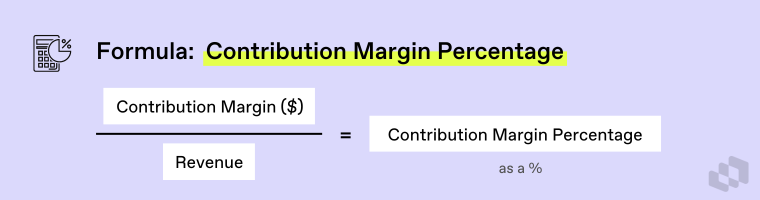

To work out the CM percentage (also known as the contribution margin ratio), you divide you contribution margin dollar value by your revenue.

The reason that is an important number is that the percentage should stay relatively consistent regardless of how much or how little we sell of our product.

Example: Contribution margin for laptops

If I’m selling 100 laptops one month and a thousand laptops the next month, typically the margin or contribution margin I’m making on each product will stay the same regardless of how much or how little I sell.

Contribution margin and economies of scale

The one thing that doesn’t take into consideration is economies of scale. Naturally if I’m running Wal-Mart or Coles or Woolworths or some big grocery store, I’m going to get a better price for my Coca-Cola than the corner convenience in store. But regardless of economies of scale, contribution margin should stay relatively consistent, and hopefully improve for your business.

How does gross profit come into it?

Gross profit is looking at your contribution margin, less your fixed costs of goods sold.

So with contribution margin, we spoke about variable cost of goods sold; with gross profit, it is looking at our fixed costs of goods sold.

They’re most likely going to be your direct labour – the people working on the job, in the factory, creating whatever you’re selling (or dispatching, in the case of a warehouse); and also the occupancy. So your factory costs, your warehouse costs; they will go under your fixed cost of goods sold. The reason being, if you were to take away the people or take away the property, you couldn’t deliver the product to your clients.

The question and variance between the contribution margin and gross profit, is it doesn’t matter how much or how little you sell in a day; you still have to pay your wages, your rent, your electricity, and all the bills associated with your property.

Summary

So, they’re the two core numbers.

Contribution margin is revenue minus variable cost of goods; and your variable cost of goods sold should shift up and down, depending on how much or how little you sell.

Gross profit is then your contribution margin, minus your fixed cost of goods sold. And your fixed cost of goods sold is your expenditure that you have to pay every day, regardless of how much or how little work they do.

Learn everything we teach our clients... free

Join 400+ business owners & leaders who receive practical business & accounting tips, delivered free to your inbox every week. No fluff, just high-level expertise. Sign up now.